India’s LPG supply crisis is expected to persist for up to four years, according to senior government officials, as ongoing geopolitical tensions in West Asia continue to disrupt critical energy infrastructure and choke key shipping routes. The prolonged instability triggered by the escalation of the US-Israeli conflict with Iran since late February has significantly impacted the Strait of Hormuz, a vital artery through which the majority of India’s liquefied petroleum gas imports are transported.

With nearly 60% of India’s LPG demand met through imports, the disruption has exposed deep vulnerabilities in the country’s energy supply chain. Officials indicate that uncertainty over damage to production facilities and gas fields in the Gulf could delay recovery timelines, with suppliers themselves warning that restoring output may take at least three years, and possibly longer.

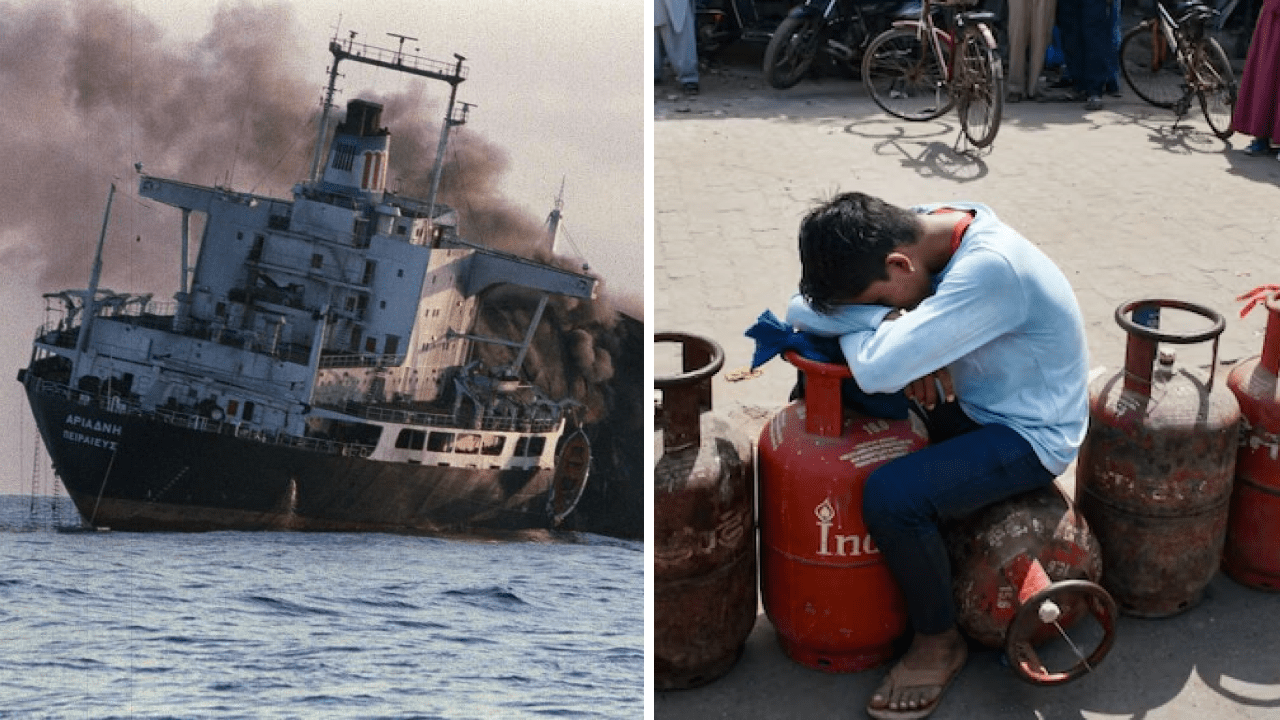

The situation remains fluid despite a temporary ceasefire, as attacks on gas processing facilities, export terminals, and associated infrastructure across the region have raised concerns about whether the shutdowns are temporary or indicative of deeper, long-term damage.

Also read: LPG Shortage in India Triggers Long Queues, Restaurant Closures and Surge in Electric Cooking Demand

Industry and Market Impact

The supply shock has already translated into higher costs for consumers and businesses across India. Prices of domestic LPG cylinders have risen by ₹60 since mid-March, while commercial cylinder rates have increased by ₹115, placing additional strain on households, restaurants, and small enterprises.

The hospitality sector, which relies heavily on commercial LPG, is among the hardest hit. Rising input costs are forcing businesses to either absorb losses or pass on price increases to consumers, contributing to broader inflationary pressures.

Oil marketing companies are also facing mounting subsidy burdens as the government attempts to shield vulnerable households from the full impact of rising prices. Meanwhile, authorities have begun prioritizing household consumption over industrial usage and have adjusted cylinder distribution intervals to manage limited supply.

Compounding the issue is India’s limited LPG storage capacity, which currently covers only about two weeks of national consumption. This leaves little buffer against prolonged disruptions, amplifying the urgency of restoring stable supply lines.

Strategic Vulnerability and Supply Chain Risks

The crisis has underscored India’s heavy reliance on West Asia for energy imports. Before the conflict escalated, nearly 90% of India’s LPG imports passed through the Strait of Hormuz. Although diversification efforts have reduced that share to around 55%, the overall disruption to supplies is still estimated at 40–50%.

Key suppliers such as the UAE, Qatar, and Saudi Arabia have all experienced varying degrees of disruption due to missile and drone attacks on energy infrastructure. Major production hubs tied to large gas fields like those in Qatar and Iran have faced operational uncertainties, further tightening global supply.

Additionally, critical export terminals and processing facilities across the region have been impacted, complicating logistics even where production remains partially intact. The interconnected nature of LPG production often linked to natural gas processing means that disruptions ripple across multiple energy markets simultaneously.

Why This Matters

LPG is a primary cooking fuel for millions of Indian households, making its availability a matter of both economic stability and social welfare. Any prolonged disruption risks widening inequality, as lower-income households are disproportionately affected by price increases.

The crisis also highlights broader energy security concerns. India’s dependence on imported fossil fuels leaves it vulnerable to geopolitical shocks, particularly in regions prone to conflict. As global energy markets become increasingly interconnected, localized disruptions can have far-reaching consequences.

Moreover, rising LPG costs could push up inflation, complicating macroeconomic management at a time when global growth remains uncertain.

What Happens Next

In response to the crisis, the Indian government is accelerating efforts to reduce dependence on LPG imports. One key strategy is promoting the transition to piped natural gas (PNG) in urban areas. Households with access to pipeline infrastructure have been encouraged to switch within a defined timeframe, with authorities planning significant investments estimated between ₹5,000 and ₹6,000 crore to expand the network.

However, progress remains gradual. As of early 2026, only about 12–13% of households are connected to PNG, indicating that scaling up infrastructure will take time.

The government is also exploring alternative energy solutions, including electric cooking appliances, biogas systems, and emerging green hydrogen technologies. While these options hold promise, they are not yet ready to fully replace LPG at scale.

In parallel, efforts to diversify import sources beyond West Asia are expected to intensify, though logistical and cost challenges remain significant.

Ultimately, the trajectory of India’s LPG supply recovery will depend heavily on geopolitical developments in West Asia. A sustained resolution to the conflict and restoration of damaged infrastructure will be critical to stabilizing global supply chains.